The Suicide Cliff: Older Western Men in Thailand

Three independent signals — Thai baseline, consular share, clinical drivers — triangulate an elevated risk band that the data systems cannot rate precisely.

Every published piece — 58 in all — filed by cluster. Start with the spine, or read by what you are afraid of.

58 pieces

The hard numbers — the math, the base rates, the costs.

Three independent signals — Thai baseline, consular share, clinical drivers — triangulate an elevated risk band that the data systems cannot rate precisely.

What an ischaemic stroke or acute coronary syndrome actually costs the uninsured Western expat at the top private hospitals in Bangkok and Manila — and why "I will just fly home" prices the wrong country bill.

Chiang Mai's air runs 3.6x the WHO limit year-round and the world's second-worst in season. Priced as a chronic dose, it costs over a year of life.

Living alone raises mortality risk by a third, and the most exposed cohort abroad is the one no dataset counts. The sourced mechanism, stated cold.

No agency counts how many retirees stay, so model it: 100 arrivals decay to 54 in place at 75, 18 at 85. The stay-curve, with its bands stated.

One legally mandated dataset of deaths abroad exists, and by statute it excludes the death the aging expat is likeliest to have. The sourced count.

At 65, a regional health plan costs about half what an international one does. The Philippines-vs-Thailand gap is real locally and gone globally. Sourced.

Healthcare costs in the Philippines climb 16% a year, in Thailand about 11% — both far above CPI. The trend rate, not today's cheap bill, decides whether the plan survives to 80.

There is no single 'FX decline' but a currency-by-country matrix, and one cell has no defence. The 18-year carry of a sterling and a dollar pension.

Two identical UK pensioners, two Southeast Asian countries, one pension frozen for life. The sourced decade of what the freeze has already cost.

No agency counts how many Western retirees leave Thailand or the Philippines. The silent cohort, triangulated from three directions, uncertainty stated.

Expat health cover is cheap while you don't need it and fails when you do. The cross-insurer age curve, and the year the premium overtakes the pension.

The retire-abroad budget is a snapshot sold as a trajectory. A transparent 25-year drawdown model, every assumption shown, the year the margin hits zero.

Insurance age-out, long-term care, and dying abroad.

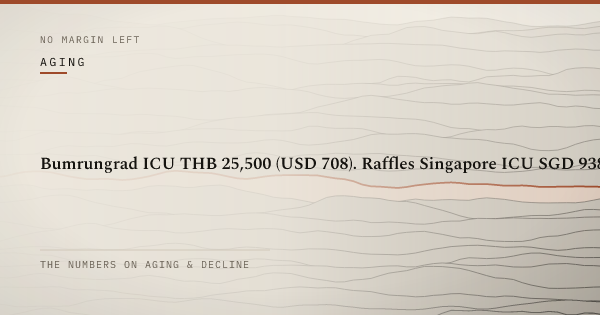

A sourced, cross-city table of standard private and ICU room rates: Bumrungrad ICU THB 25,500, Raffles SG ICU SGD 938, Lam Wah Ee Penang ICU MYR 320. And why the rate card is 25 to 35% of the actual bill.

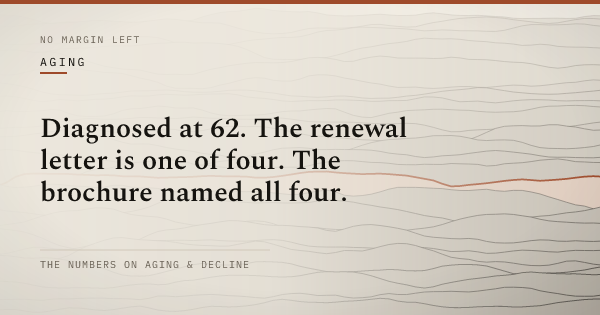

The IPMI brochure says renewable to 99. The renewal letter, after a Type 2 diabetes diagnosis at 62, says four things instead. None of them say the brochure was wrong.

Verified 2026 air-ambulance route prices, what IPMI evacuation cover actually does (Singapore, not home), the age curve that thins at 75 and dissolves at 85, and the line where evacuation is the wrong call.

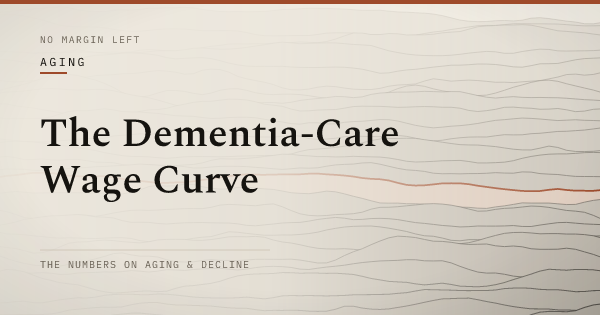

Chiang Mai dementia care at $2,400-4,400/month is a snapshot of a curve. Statutory floor, nurse shortage, domestic demand, and the absence of insurance backstop projected to 2035.

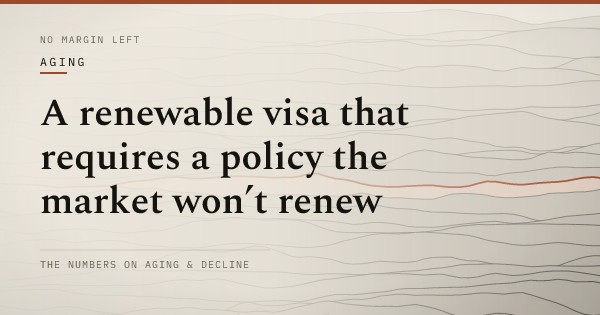

Thailand’s O-A retirement visa requires a policy the market is least willing to write. The OIC-approved insurer × age × certificate matrix, and what the renewal week actually looks like at 71, 74 and 76.

A younger wife lowers a husband's mortality by about 11%. The same study finds she pays for it in her own life expectancy. The actuarial case.

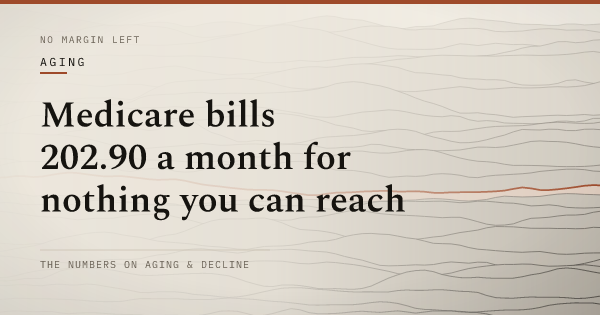

Medicare pays nothing where you live but still bills $202.90 a month; the NHS ends the day your move is permanent. Two systems, two failure modes, sourced.

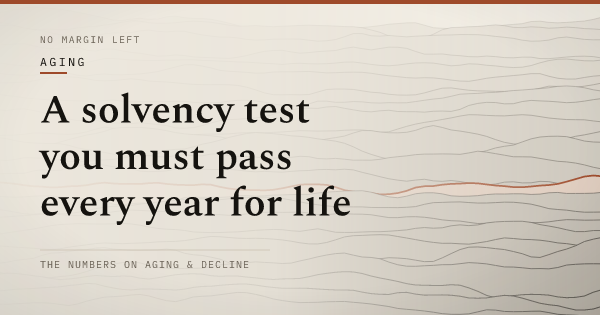

The O-A visa is not a one-time hurdle but a three-gate solvency re-test run every year for life, each gate hardening with age. Decomposed and costed.

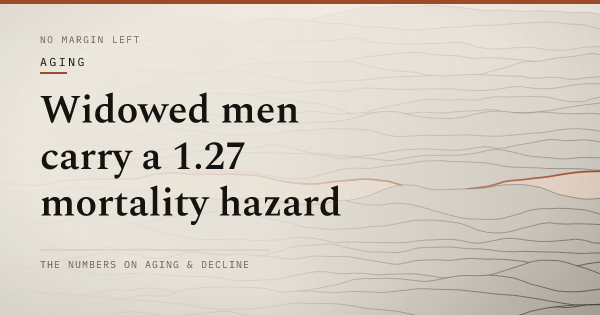

Widowed men carry a mortality hazard around 1.27, peaking near 1.41 in the first six months. Abroad and alone, every buffer the figure assumes is gone.

Sending a body from Thailand to the USA runs $10,000-$20,000 all-in, over 6-13 weeks, under a 30-day clock. The repatriation runbook, costed by leg.

The isolation-to-dementia science is settled; the living-alone risk is documented. The move abroad raises that risk and removes the detection.

A live-in carer in Thailand or the Philippines costs under US$600 a month. The number is real, and it answers the wrong question. The care ladder, costed.

Cheap care is a per-month number. What ends estates is duration: a multi-year dementia trajectory, paid uninsured, with no one to hold the tier down.

A Thai private hospital wants 50,000-200,000 baht in cash before it treats you. The cost ladder of one uninsured emergency, and the medevac tail beyond it.

Rejection at 75 starts a forced choice among four paths, one of them deliberate uninsurance in the highest-risk decade. The matrix, costed.

'Lifetime renewable' reads as a safety net. Across insurers it is a deadline: who accepts you, until what age, on what condition. The matrix.

What relocation does not fix — the ideas behind the numbers.

He arrived projecting capability. The body is the audience that stopped clapping. SE Asia is the stage that was always going to outlast the actor.

A form of capital that is not money, not friendship, not language. It is the accumulated record held in the minds and files of an institution-rich locale. Relocation severs it.

"It's so cheap here" is a snapshot taken at the lowest-cost point of a life. The three forces that compound upward as the body declines, and what cheapness costs.

The general case is that you take yourself with you. This is the itemised one: loneliness, a failing marriage, drinking, depression, money fear — each tied to the data showing it stays broken.

The retire-abroad channels you watch are made, by construction, by the people for whom it worked. The ones it broke don't post a final video. The denominator is missing.

The universal expat reassurance is a conditional that fails exactly when it is needed. 'Go home' decomposed into five preconditions, each plotted.

The expat second-year wall is real, but the culture-shock U-curve that explains it fails its own tests: a novelty dividend amortising to zero.

For many, isolation in late life abroad is not a risk of the move but the structural endpoint of it. Each support decaying on age, distance, foreignness.

The brochure footage is real, and honeymoon-phase, survivor-sampled data sold as a marriage. Paradise is a relation, and the move ends it on schedule.

Moving abroad won't make you happy. The geographic cure is a term from addiction recovery. What travels with you, what doesn't, when the bill lands.

Visa-income math and the pre-move reality-check.

What the Philippine Retirement Authority actually did on 1 September 2025 — categories collapsed, deposits raised, age dropped, and the peer-program floor after Malaysia tightened first.

Thai tax residence turns on a calendar count, not a status. The 180-day threshold, the day-counting rule, the three responses to it costed honestly.

A foreigner can buy the house and never own the land under it. What each workaround signs away when the marriage or the law turns, costed.

Conventional planning stress-tests against a market crash. For an aging expat the plan-ending shocks are certain and permanent: cliff, care tail, freeze.

A monthly cost figure is the wrong tool for a 25-year retirement. The reproducible 7-step method for your own year-the-margin-hits-zero, levers ranked.

Every retire-abroad checklist is built to clear you to go. This one can return 'no': four solvencies, financial to exit, scored on 25-year survival.

The '$10,000 SRRV' every guide quotes was abolished in September 2025. What the restructured visa now costs to enter and hold, by age, sourced.

The 65,000-baht income rule is pre-tax, single-person, and cheapest-city, and the qualifying remittance is itself the taxable event. Modelled by FX.

Average UK rent alone is about 131% of the full state pension. 'I'll just go home' is the fallback nobody costs, and its price rises every year abroad.

Thailand's 2024 remittance tax treats pensions differently. A double-tax treaty decides whether yours is assessable at all, by its character, not its size.

Philippines and Thailand reality files.

HCMC is the cheapest of the launch cities on the daily basket and the structurally hardest to age in. The slow VND tailwind does not save it. The visa stack, the frozen UK pension and the friction stack do the work.

Vietnam is the only ASEAN-6 mainland country without a statutory retirement visa. The realistic stack costed honestly, plus the 2028 sunset risk no one mentions.

A ฿1,200 night out in Pattaya, a ₱2,000 one in Angeles. The daily number is small and true. Compounded over ten years, here is the six-figure total the daily number hides — and the health cost beside it.

The cheap-living city and the best-care city are not the same one. Bangkok vs Chiang Mai on the access dimensions that decide outcomes with age — and the transfer.

Cebu has good hospitals. All seven of the Philippines' JCI-accredited facilities are in Metro Manila. For the rarest emergency at the worst age, the gap is the plan.

Bangkok has the highest retiree baseline of the four launch cities and Asia's best private hospitals. Run as a 25-year trajectory, that combination is why the money runs out faster here.

Chiang Mai sells the lowest burn in the brochures, near $1,500 a month. The honest figure is the crossover age — a frozen pension and a flat baht pull it in.

Manila is the most expensive of the launch cities, about US$200 a month over Cebu. Run the trajectory to the year the margin hits zero — and what the premium buys.

A single retiree can live in Cebu City for about $1,400 a month. That number is real, and it has an expiry date. The Cebu cost-of-aging trajectory, run to the year the margin reaches zero.

Nothing matches that. Clear the filter, or search the full text.